What are the pros and cons of USDA loans and where can I use a USDA loan in the DMV area?

TLDR

- USDA loans offer zero down payment with competitive insurance, expanding suburban affordability.

- Eligibility depends on income limits and property location outside dense urban cores.

- Best DMV fits include Stafford, Spotsylvania, Fauquier, Loudoun fringes, and outer Maryland suburbs.

- Preparation matters: strong preapproval, timeline awareness, and local guidance speed smooth closings.

What do USDA loans really mean for DMV buyers?

USDA loans are government-backed mortgages designed to make homeownership possible in rural and select suburban communities. In the DMV, they are a powerful tool for buyers who want more space, newer construction, and manageable monthly payments while avoiding a down payment. With the market normalizing in 2025, median days on market across the region hover around 30 to 45 days, and price growth has cooled to roughly 3 to 5 percent. That creates a more approachable runway for financing choices like USDA alongside conventional, FHA, and VA options. Regional medians sit near $640,000 in Washington, DC, about $550,000 across key Maryland suburbs, and roughly $625,000 in Northern Virginia, based on recent MLS reporting.

Near my office at 800 Maine Ave SW, neighborhoods like The Wharf, Southwest Waterfront, Navy Yard, and Capitol Hill remain anchored in the urban core. These areas are generally not USDA eligible. Many of my clients who work near the Wharf choose a USDA-eligible suburb where they can enjoy larger homes and yards, then commute in by car, VRE, or MARC depending on their location and schedule.

Here is how I define it as Kelly Jackson:

- A smart path to homeownership with zero down, often at a lower monthly cost than renting.

- A way to expand your home search beyond the Beltway while maintaining reasonable commutes.

- A lending option that rewards stable income, responsible credit, and property eligibility.

How do USDA loans work in the DMV?

USDA Guaranteed loans allow qualified buyers to finance up to 100 percent of a home’s purchase price in eligible areas. The program’s mortgage insurance cost is competitive, with a 1 percent upfront guarantee fee that can be financed and a 0.35 percent annual fee, often resulting in a lower overall payment than comparable low-down-payment options. Household income is typically capped at 115 percent of the area median income, which varies by county. For context, typical caps in our region often fall near six-figure thresholds, so many middle-income households qualify.

Property eligibility is defined by the USDA’s map, which does not include any sites within DC boundaries. Much of suburban Maryland and Virginia beyond the immediate I-495 corridor includes eligible tracts. Timelines are comparable to other loans. Most buyers close in 30 to 45 days once they are fully under contract and underwriting receives final documentation.

You can learn program specifics at the USDA’s official page and verify addresses using the agency’s map:

Eligibility basics: income, credit, and property

- Income: Household income typically cannot exceed 115 percent of the local AMI. Example caps in our region often approximate $145,000 in higher-cost Maryland counties and up to about $160,000 in select Northern Virginia counties, with lower thresholds near $108,000 in Stafford County. Always confirm current limits at the USDA site.

- Credit: Many lenders look for a 640 score for streamlined underwriting.

- Property: The home must be your primary residence and located in an eligible tract per the USDA map.

For regional market context and pricing, see Bright MLS Market Data for quarterly updates.

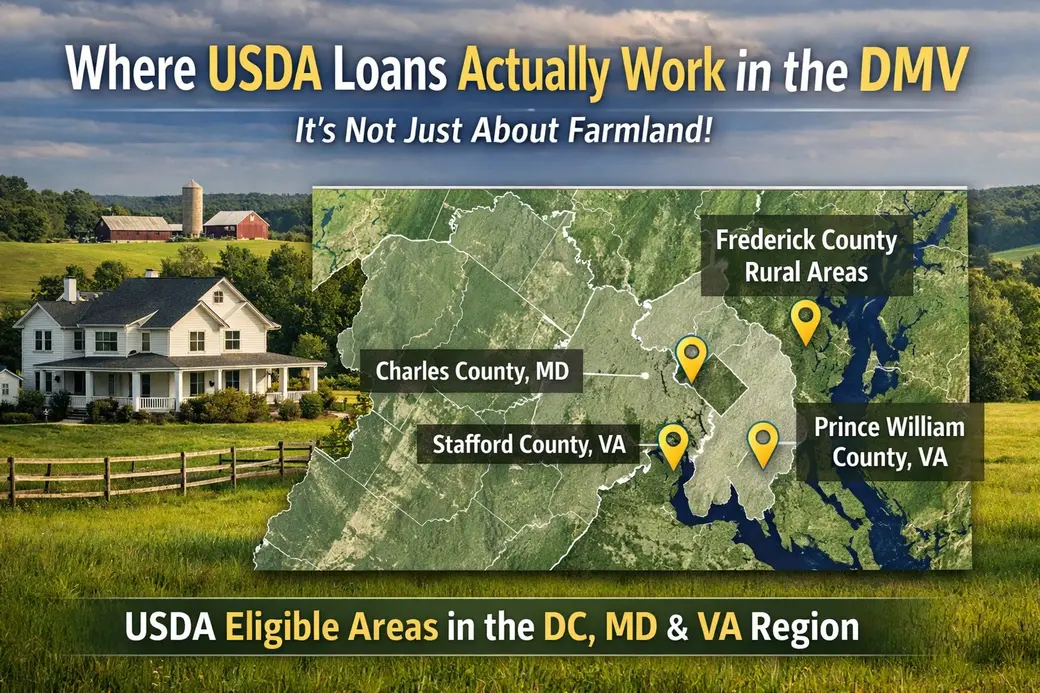

Where can I use a USDA loan around DC, Maryland, and Virginia?

If you love the Wharf, Southwest Waterfront, Navy Yard, or Capitol Hill for work and entertainment, USDA financing is your ticket to more space just beyond the urban core. In Virginia, eligible tracts are common in Stafford, Spotsylvania, and Fauquier, plus portions of Loudoun and the rural fringe of Fairfax north of Route 50. In Maryland, look to Charles, Calvert, and many parts of Prince George’s and Anne Arundel outside I-495. Frederick County real estate also includes large pockets with potential eligibility, especially as you head away from the City of Frederick.

Think in terms of commute corridors. From Stafford and Spotsylvania, VRE stations create reliable links to the District. In Maryland, MARC lines and park-and-ride lots support predictable travel. For school-minded buyers, counties like Montgomery and Fairfax remain top-ranked, but USDA opportunities expand as you move outward to neighboring communities, where new developments often deliver larger lots and newer builds.

Neighborhood 1: Stafford County, Virginia

- Details: Popular communities include Embrey Mill and areas near Brooke Station. Newer homes, community pools, and trails offer strong value. - Watchouts: Some HOAs have amenity fees. Confirm USDA eligibility by address and review well and septic inspections where applicable. - Typical timeline: Preapproval within a week, home search 2 to 4 weeks, 30 to 45 days to close.- Neighborhood 2: Frederick County, Maryland

Other targets for USDA loans in the DMV include Nokesville in Prince William County, parts of Southern Prince George’s like Brandywine and Accokeek, and Calvert County towns such as Prince Frederick. If you track Prince William County real estate, know that eligibility widens as you move southwest toward rural zones. Always use the USDA map to confirm property-level qualification.

What are the pros and cons of USDA loans?

Pros:

- Zero down payment, which preserves cash for reserves, repairs, and furnishings.

- Competitive monthly cost, thanks to a modest 0.35 percent annual guarantee fee.

- Flexible credit requirements with manual underwriting pathways for near-miss files.

- Ability to finance the 1 percent upfront guarantee fee into the loan amount.

- Often lower total monthly payment than low-down conventional or FHA in eligible areas.

Cons:

- Geographic restrictions limit eligible properties, with no eligibility inside Washington, DC.

- Income caps at 115 percent of AMI can exclude higher earners in costly counties.

- Longer underwriting in peak seasons if the lender has heavy USDA volume.

- Appraisal and property standards may flag condition items, which can extend timelines.

How do I prepare, budget, and close on a USDA loan in the DMV?

Start with a detailed preapproval that verifies income, credit, and assets. Ask your lender to run a USDA-specific scenario so you understand the upfront guarantee fee, monthly fee, and total payment. Typical buyer-paid costs include appraisal (about $600 to $850), home inspection packages ($500 to $800 depending on add-ons like radon or sewer scopes), and standard lender and title charges that can total 2 to 3 percent of the price. In a balanced market, it is often possible to negotiate seller credits to offset part of these costs.

I help clients match search areas to commute needs and loan rules. For families in the DMV area, we often tour in Stafford, Spotsylvania, Frederick, St Mary's, and southern Prince William County to keep commutes manageable. If schools drive the decision, we compare county programs and leverage publicly available data, such as NCES district profiles, while advising on local nuances.

One of my clients was a first-time buyer who worked at L’Enfant Plaza. We targeted Brooke Station in Stafford for VRE access and found a three-bedroom townhome for $400,000. With USDA financing, zero down, and a modest seller credit, their cash to close was under $10,000 including reserves, and we closed in 34 days. Another client, a remote worker, favored Frederick County for larger lots. We confirmed eligibility outside the City of Frederick, used USDA plus lender credits, and secured a single-family home with a monthly payment below their rent.

To compare programs, I often pair USDA with local aid when available:

- DC Open Doors for buyers purchasing in the District, if USDA is not an option.

- Maryland Mortgage Program for down payment assistance when USDA does not fit.

- Virginia Housing MyHome for qualifying Virginia buyers.

If you plan to sell home in Stafford County and then buy with USDA nearby, we can coordinate list timing to align with your purchase. For sellers, monitor county-level inventory and pricing via Bright MLS Market Data and county planning updates like Stafford County Planning.

FAQs

1) What is the real monthly cost difference between USDA and FHA? USDA’s 0.35 percent annual fee is typically lower than FHA’s annual MIP. USDA also allows zero down, which affects financing structure. In many eligible areas, USDA results in a lower overall payment for the same price. The best comparison uses a live rate quote and current insurance factors from your lender, plus taxes and HOA.

2) Can I use USDA for a condo or townhome? Condo and townhome purchases can qualify if the property sits in an eligible tract and meets USDA standards. The condo association must be financially stable, with adequate reserves and no litigation. Some attached homes share utilities or infrastructure, so your appraiser and underwriter will review documents carefully. Always verify eligibility by address using the USDA map before writing.

3) How strict are the income limits in our region? USDA uses household income and caps it at around 115 percent of AMI. Caps vary by county and household size. In practice, limits often range from near $108,000 in Stafford County to around $145,000 or higher in select Maryland counties and up to about $160,000 in certain Northern Virginia counties. Check the current figures on the USDA site and with your lender.

4) Is there any USDA eligibility inside Washington, DC? No. The District is fully excluded on the USDA eligibility map. Buyers who want the Wharf, Navy Yard, Southwest Waterfront, or Capitol Hill should consider conventional, FHA, or VA loans or leverage local assistance like DC Open Doors. If zero down is a priority, we can identify nearby eligible suburbs with reasonable commutes into the city.

5) How long does a USDA loan take from contract to closing? Typical timelines run 30 to 45 days, similar to conventional and FHA. Preapproval should be completed before offers. Appraisal, title, and underwriting drive the schedule. In peak seasons, USDA underwriting volume can add a few days. Planning inspections early, responding quickly to document requests, and using experienced local lenders reduces surprises and keeps closings on track.

6) Can I roll closing costs into a USDA loan? USDA does not normally finance closing costs into the base loan. However, if the appraised value is higher than the purchase price, some lenders allow financing of the guarantee fee and possibly a portion of closing costs within that appraised margin. Many buyers negotiate seller credits or apply lender credits to reduce cash to close while keeping payments comfortable.

7) What should I know about schools and amenities in USDA-eligible areas? Many eligible areas are suburban communities with strong amenities like parks and trails. Families often explore county school data using resources like NCES. For example, Fairfax and Montgomery remain highly regarded, while neighboring counties offer solid value and growing amenity sets. We compare commute patterns, school considerations, and resale outlooks so your USDA purchase supports long-term goals.

Conclusion

The bottom line USDA loans unlock zero-down financing that fits many buyers seeking space and value just outside the Beltway. In a balanced 2025 market, they can deliver lower monthly costs than other low-down options, provided you meet income and location guidelines. In Virginia, focus on Stafford, Spotsylvania, and Fauquier, with pockets in Loudoun and rural Fairfax. In Maryland, look to Charles, Calvert, parts of Prince George’s and Anne Arundel, and areas across Frederick County real estate. If you want the best usda realtor experience, I will help you match neighborhoods, commute routes, and financing options so your purchase is confident and smooth.

Categories

- All Blogs (111)

- Affordability and Cost of Living (13)

- Andrews Air Force Base (3)

- AS IS Home Sale (3)

- Baltimore County Real Estate (1)

- Baltimore Homes (2)

- Baltimore Real Estate (2)

- Buyer Education (5)

- Buyer Guides (15)

- Buyer Representation (2)

- Buyer Resources (4)

- Buyer Strategy (11)

- buying a home (8)

- Buying a Home Near DC (6)

- Camp Springs Real Estate (1)

- Capitol Hill DC (3)

- Charles County MD (4)

- Charles County Real Estate (4)

- College Housing Strategy (1)

- Condo & Co-op Living (2)

- Condo Living (5)

- DC Commute Times (2)

- DC Home Values (6)

- DC Market Trends (6)

- DC Neighborhood Insights (9)

- DC Neighborhoods (12)

- DC Real Estate Market (24)

- DC Relocation (6)

- DC Waterfront (1)

- DMV Buyer Strategy (9)

- DMV HOAs (3)

- DMV Housing Market (6)

- DMV Market Guides (2)

- DMV Neighborhoods (7)

- dmv real estate (23)

- Dumfries VA Real Estate (2)

- Expired Listings (1)

- Fairfax County Real Estate (2)

- Financing & Mortgage Guidance (1)

- First Time Home Buyers (4)

- Fort Belvoir (1)

- Fort Detrick Military Relocation (5)

- Fort Detrick PCS (5)

- Fort Washington MD (2)

- Fort Washington MD Real Estate (1)

- Frederick County Real Estate (3)

- Georgetown DC Realty Estate (1)

- Historic DC Communities (1)

- Home Buying Advice (4)

- Home Buying Education (2)

- Home Buying in Washington DC (8)

- Home Buying Strategies (2)

- Home Buying Tips (2)

- Home Improvement ROI (2)

- Home Prep (1)

- Home Preparation for Selling (1)

- Home Selling Advice (11)

- Home Selling in Washington DC (12)

- Home Selling Process (2)

- Home Selling Strategy (8)

- Home Selling Timelines (5)

- Home Value & Pricing (1)

- Home Value Pricing & Strategy (1)

- Home Value Trends and Forecast (1)

- House Hacking & Investment (1)

- Investor Education (1)

- Local Market Insights (2)

- Luxury Adjacent Homes (1)

- Luxury Home Selling (1)

- Market Conditions (1)

- Maryland Communities (10)

- Maryland Home Buyers (15)

- Maryland Home Sellers (16)

- Maryland Home Values (1)

- Maryland Homeowners (5)

- Maryland Neighborhoods (11)

- Maryland Real Estate (30)

- Montgomery County MD (8)

- Montgomery County MD Housing Market (6)

- Mortgage and Financing (2)

- National Harbor MD (1)

- Neighborhood Guides (8)

- Net Out Sheet (1)

- New Construction Homes (1)

- Northern VA Home Buyers (17)

- Northern Virginia Buyers (14)

- Northern Virginia Home Sellers (22)

- Northern Virginia Real Estate (34)

- Oxon Hill MD (1)

- PCS Housing Guide (5)

- Petworth DC Home Prices (1)

- Petworth DC Real Estate (2)

- PG County Real Estate (6)

- Prince George’s County Real Estate (11)

- Prince William County Real Estate (5)

- Real Estate Advice (2)

- Real Estate Closings (1)

- Real Estate Contracts (1)

- Real Estate Market Insights (4)

- Real Estate Negotiation and Strategy (2)

- Real Estate Strategies for Home Sellers (8)

- Reat Estate Strategy for Sellers (6)

- Relocation & Moving to Northern Virginia (16)

- Relocation and Military Housing (17)

- Rockville MD Real Estate (1)

- Sell Maryland Home (7)

- Seller Education (13)

- Seller Resources (6)

- Seller Strategy (14)

- Seller Success Stories (1)

- Silver Spring Real Estate (2)

- Smart Buying Strategies (2)

- Southern MD Real Estate (2)

- Stafford County Real Estate (3)

- student loans (1)

- Triangle VA Real Estate (1)

- USDA Loans DMV (1)

- VA Home Loans (2)

- VA Loan Purchase (2)

- VA Market Insights and Trends (4)

- Virginia Home Selling Guide (3)

- Washington DC Real Estate (19)

- Washington DC Sellers (7)

- Wealth Building (1)

- Where to Live in Northern Virginia (8)

- Woodmore MD (1)

- Zero Down Payment Programs (1)

Recent Posts